Tiger Kahan Hai?

Feb 4, 2023

Hey folks,

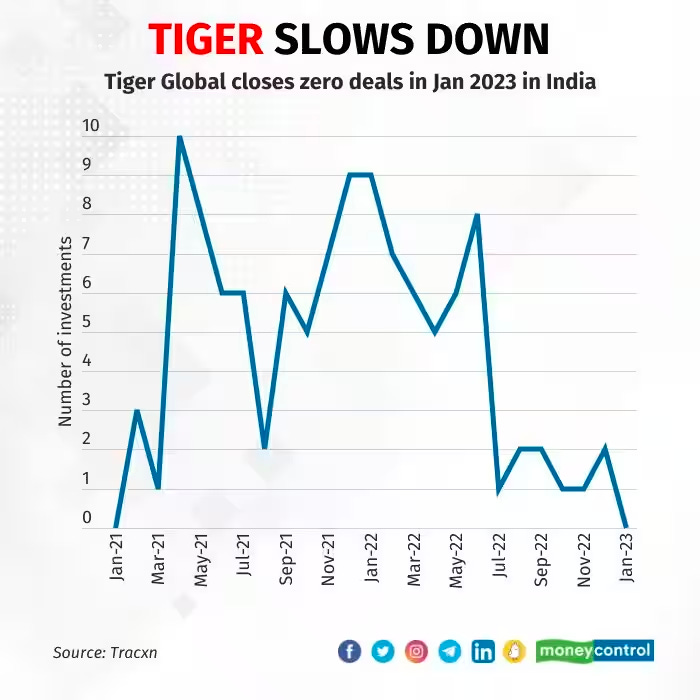

We’re back to covering everyone’s favorite investor in India, Tiger Global, and what the future might hold for the Indian ecosystem. Earlier last week, MoneyControl reported that January 2023 was the first time Tiger didn’t write a single investment in an Indian company. While Tiger and other global investors were writing checks every week during the heyday of the pandemic, that has come crashing down in the latter half of 2022 and as we move into 2023. This, for Tiger, is neither an India-only phenomenon as their global investment velocity has slowed down significantly nor is it something they haven’t done in India in the past. We wrote back in April 2021, when Tiger coined 4 new unicorns in India (CRED, Groww, ShareChat and GupShup):

“The thing about Tiger Global, though, is that the firm has been quite hot and cold with its investments in the country. Every cycle, it starts off being very aggressive and does a bunch of deals and investments for a couple of years and then goes dormant for a few years. The Indian market saw this when Tiger was very aggressive in 2014 and 2015 (according to Crunchbase, Tiger participated in 46 funding rounds), but then was fairly quiet in 2016, 2017 and 2018 having only participated in 12 funding rounds in those 3 years. The firm has certainly been active in 2019 and the early parts of 2020 but seems to have gotten even more aggressive in the last two quarters. Is it still yet to be seen how long Tiger truly will be active in the country given that historically India hasn't really generated a lot of returns for the firm.”

Amidst these struggles, their longtime partner John Curtius left the firm late last year, and the firm recently is scaling down the target for their newest fund which they may have struggled to raise. The firm’s absence from India as a combination of all these factors doesn’t come as a surprise - as corrections in the public markets have left growth investors slowing down their investment pace, they have understandably pulled back from India and other emerging economies. Tiger has traditionally invested heavily in the SaaS and Fintech sectors, however, recent regulation from the RBI and the departure of John Curtius, who led a lot of their SaaS investments in India, have also contributed to their decreased activity in India.

In a rare public appearance on a panel hosted by Matrix Partners India, Scott Shleifer spoke about the firm’s history in India and their continued belief in the Indian markets and founders. Scott was quite frank and open about how returns in India have historically “sucked” for the firm, and this was the key quote from the entire panel:

“Our returns in India, our IRR, is something like 20% gross since inception. That compares to mid-30s in the U.S. on the private side, and low-50s in China. But that’s the past.”

Paraphrasing Scott, I have heard for the last 10 years from Indian investors that returns have historically not been great in the subcontinent but that it’ll get better and improve. And every couple of years I ask them when? The pandemic fueled free-money era is not returning and it raises a key question about Indian companies being able to go public in future. Growth rounds in the country have stagnated, and while things haven’t impacted the early stages as much the ecosystem risks another couple of years where Series B/C+ rounds become hard to come by and a lot of companies (great and bad) die out. This is similar to the capital influx in 2015 and capital flight in 2016, which was partially attributed to Tiger, as acknowledged by Scott.

The bet on India and Indian companies has been a bet on India’s macro-economic outlook with a massive population that is coming online in an ever increasing rate. The number of India’s internet users looked vastly different in 2010 when Tiger first wrote an $8M check into Flipkart. But even with >600M internet users in the country, Tiger and other global investors have fared better in other markets. Investors in India often mention the need for patience with companies as they take longer to become profitable, go public, and deliver returns. But venture firms investing in India have to eventually show that their investments in the country result in actual cash returns rather than just other investors marking up their investments. A couple years ago, Karthik Reddy (Managing Partner at Blume Ventures) penned this 3-part piece on the need for Indian companies to list publicly, and he makes a great point why Indian companies and firms need public exits- "no legendary Fund Vintage cycle is created without enough quality IPOs". And after more than a decade, the question remains whether global investors will lose patience with the Indian market or if companies will prove them wrong and deliver great outcomes.

Other stories we have been following

Startups were noticeably absent from this year’s union budget as the dreaded angel tax is returning which might lead to foreign investors finding it harder to invest in Indian companies or drive Indian founders from choosing to incorporate their companies elsewhere.

The latest on Adani and Hindenburg: After becoming the richest man in Asia, a report by the research firm and short seller Hindenburg has sent the shares Adani Group spiraling downwards.