A NUE payments player on the block

5th April

Hi folks, Vedica here with the newsletter today. Anmol and I both have to apologize for being AWOL from Substack for the last few weeks. Real life getting in the way ☹️ But we are back to more regular programming, with an overview of NUE, news of the week and the regular good stuff.

Can NUE take on UPI?

We have written a lot about how digital payments have taken off in India thanks to UPI - Unified Payments Interface - the rails that most of the country now transacts on. The real-time payment system was developed by National Payments Corporation of India and is regulated by the Reserve Bank of India.

Last year, the RBI issued guidelines for possible new umbrella entities - NUE(s) - that would be allowed to set up and operate payment systems manage payment systems and compete with the NPCI.

Yesterday was the last day for entities to apply for authorisation as a NUE under the RBI's mandated framework. So, we thought this is an appropriate time to talk about why exactly the RBI wants to go down this path.

Let's start with a bit of history. In 2008, the pre-Jio era when digital transactions were really the outlier in India, the RBI and the Indian Banks' Association (IBA) got together to set up the NPCI, a not-for-profit organisation, to facilitate digital payments and build the necessary infrastructure for these.

The most famous of these is UPI, which was launched in 2016, and enables peer-to-peer interbank transfers. In addition to UPI, the NPCI also manages and supports FASTags, NEFT, Aadhaar-enabled payments, IMPS, ATM transactions and the RuPay card.

The NPCI though isn't a government or public body - in fact, it steadfastly maintains it is not. The organization is managed by a consortium of 56 public and private banks, and it is this status that has caused some concern to the RBI.

In a 2019 policy paper, the RBI warned that the NPCI's singular status as the sole manager of digital payments infrastructure in India was problematic. The paper stated this problems:

a) Systemic and Operational risk: Possibility of single point of failure and also makes the entity too big to fail.

b) Lack of innovation and upgradation: Inadequate competition resulting in complacency as there is no need for constant upgradation and innovation in products and processes for retaining the customers.

c) Inefficiencies: Monopolistic trends may negatively impact customers on charges, access, quality of service, etc

UPI transactions have been growing at a breakneck speed, with transaction volume in March hitting ₹5Lcr (~$69B). In addition to the NPCI being the sole administrative body, PhonePe, GooglePay and Paytm accounted for a value share of 94.5% of these transactions. So the need to inject more competition in the space does make sense. Especially since there have been issues with rejected transactions etc. on UPI.

The RBI believes that establishing NUE (or NUEs; the body has been obscure about whether it will grant one license or two) could accelerate innovations in payments and give users alternatives to NPCI. In line with this aim it has mandated that the network and system that the new entities develop should interact with NPCI's systems and be interoperable.

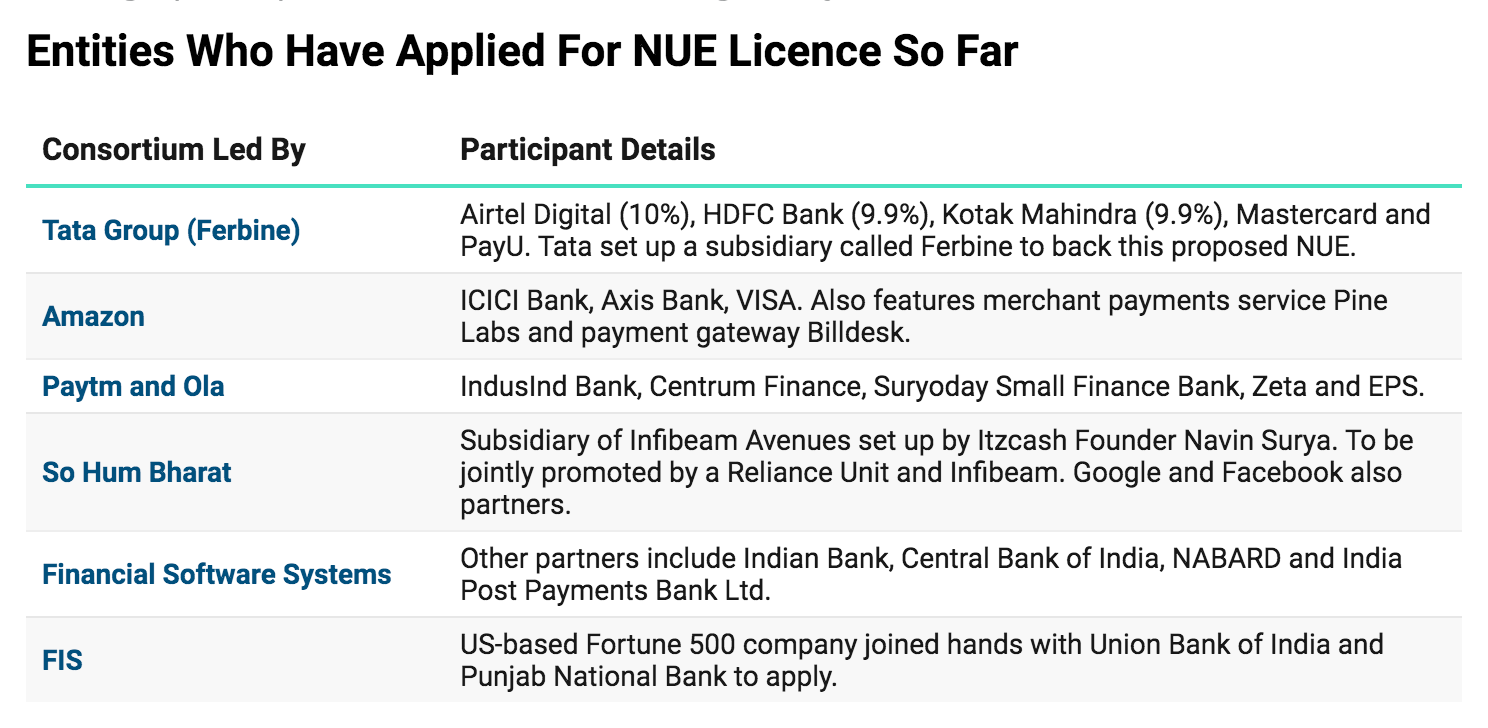

So far six entities have applied for a NUE license (source: Transfin). A lot of the names on the list should not be a surprise. Players like Amazon and Reliance clearly want a share of the growing digital transactions pie, and this ties in nicely with the e-commerce aspirations. The same goes with the other financial institution players who were clearly caught off-guard by UPI's success.

How NUE will develop and whether it will take off is of course to be seen. But it is definitely a story to keep an eye out on, because it is likely to have repercussions on the next stage of digital transactions in India.

🗞️ News of the week

Several private equity investors (TPG, ChrysCapital and Premji Invest) have invested ~$315M in FirstCry, which now values the omnichannel player at around $2B. A majority of this transaction ($300M) was secondary aka new investors bought out of the stakes of the early investors.

Hyperlocal delivery startup Dunzo has raised an additional $8M in an ongoing Series E. The company is now valued over $300M. The company has certainly had its ups and downs over the last couple of years but has now doubled it's annual active user base from 2019 to 2020.

Amazon has acquired Perpule, a startup that is helping offline stores go online. Perpule, which had raised $6.36 million, offers a mobile payments device (point of sale machine) to offline retailers to help them accept digital payments and also establish presence on various mini app stores including those run by Paytm, PhonePe and Google Pay in India.

Byju's is in talks with online reading platform Epic. The startup offers unlimited access to over 40,000 books, videos and quizzes from more than 250 publishers to kids aged 12 or younger.

Last week, a hacker claimed that they had access to 8.2 terabytes of MobiKwik's users' data (including phone numbers, email addresses, hashed passwords, transactions logs and partial payment card numbers, etc.) This is not Mobikwik's first breach, but the company is still sticking to its claim that the data had not leaked from their end.

The short video (and also social commerce) platform Chingari announced that they had raised $13M in a new financing round led by OnMobile. The round also saw Bollywood star Salman Khan join the cap table of the company - he was allotted <$2M worth of shares for being the brand ambassador of the platform.

📰 What we've read and listened to this week

A Taiwan Crisis May Mark the End of the American Empire by Niall Ferguson

A Chat with Semil Shah, Founding General Partner of Haystack by Sarthak Haribhakti

The Big Lessons of the Last Year by Morgan Housel

The Mythology of Red Bull by Mario Gabriele

🎙️ Podcast of the week: Renegades: Born in the USA

A really great series of conversations between Bruce Springsteen and Former Prez Obama. I loved the episode on Money and the American Dream.